More and more countries are requiring companies to exchange invoices electronically. In doing so, they are laying the groundwork for government VAT reporting systems (e-reporting) designed to reduce fraud. E-invoicing and e-reporting follow specific patterns, or models, that define how businesses and platforms communicate with each other. Two of these models are especially worth understanding.

Contents

- Key players in e-invoicing and e-reporting

- Trends in e-invoicing models

- The 4-corner model: a standardized e-invoicing process

- The 5-corner model: including e-reporting

- DocuWare – future-proof for every model

Key players in e-invoicing and e-reporting

A variety of models for electronic invoice exchange and digital tax reporting (e-reporting) have become established around the world. They differ primarily in the participants involved in the process and the role played by the tax authority. The participants in these models are referred to as “corners.”

Every invoice exchange involves at least the supplier (the invoice sender) and the buyer (the invoice recipient). An additional participant is the tax authority, although one model operates without its involvement.

When invoices are exchanged through a network such as Peppol, the network’s access points are also involved. These platforms not only manage invoice transmission but also perform additional tasks, including validating invoices, reporting their status, and converting one country’s invoice format into another – for example, converting an Italian FatturaPA invoice into a German XRechnung.

Trends in e-invoicing models

Some countries, such as Italy and Hungary, use the 3-corner model. In this approach, invoices are first submitted to a government platform for validation and approval before they can be delivered to the recipient, a system known as the clearance model.

However, network-based models with four or five corners are becoming increasingly important. These models rely on a standardized network – such as Peppol – for the secure exchange of invoices between businesses or between businesses and government authorities. In the 4-corner model, the sender and recipient exchange invoices through their respective network access points. The 5-corner model builds on this approach by adding the parallel reporting of tax-relevant invoice data to the tax authority – a process known as e-reporting.

These two models currently form the basis of many national e-invoicing initiatives and are therefore explained in more detail below.

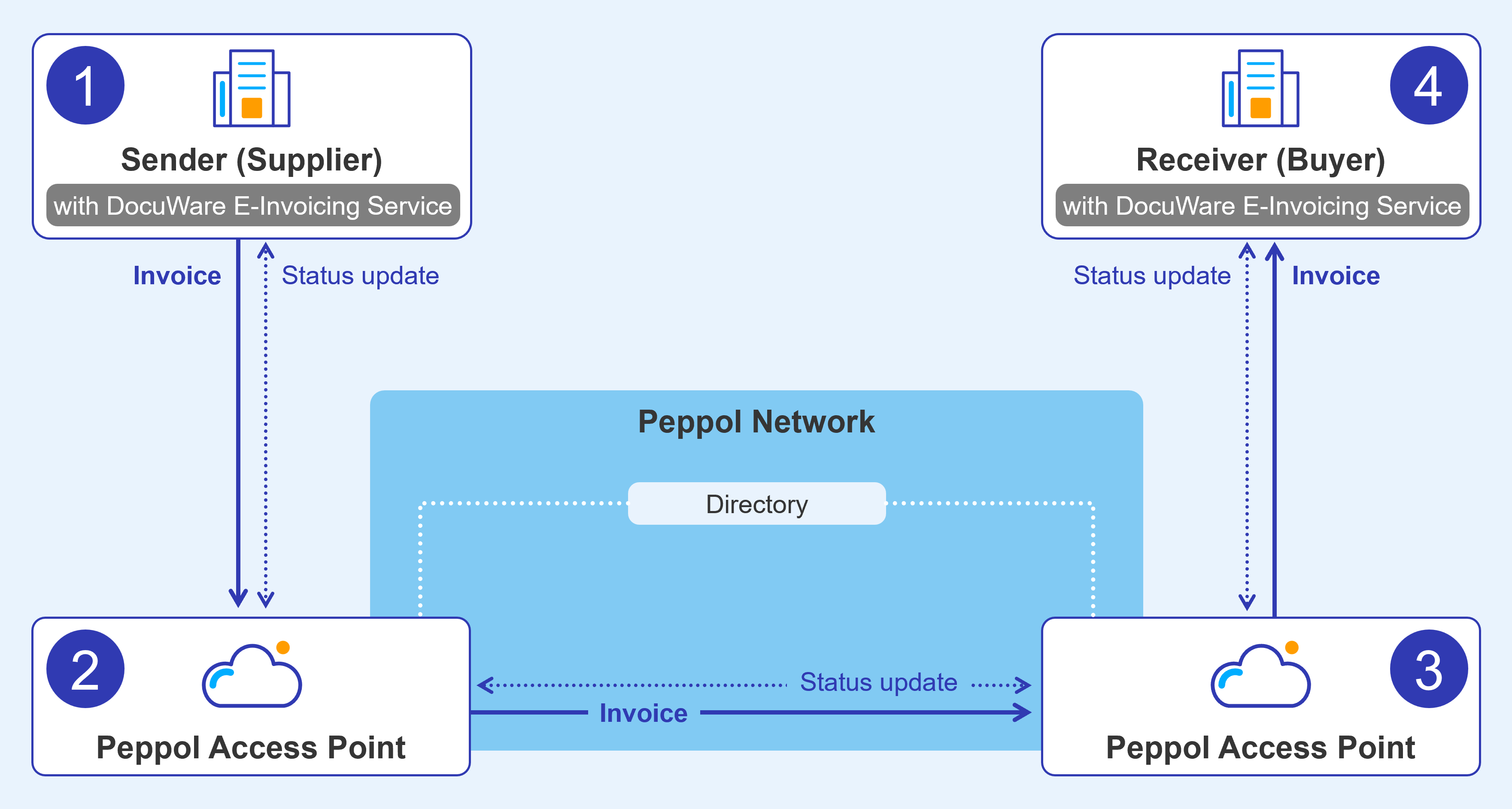

The 4-corner model: a standardized e-invoicing process

The participants in the 4-corner model are:

- Supplier (sender)

- Peppol Access Point chosen by the supplier

- Buyer (recipient)

- Peppol Access Point chosen by the buyer

The supplier creates the electronic invoice in the format required by its country – for example, XRechnung in Germany or KSeF in Poland. The invoice is then transmitted to the supplier’s Access Point, typically through an automated process. With the DocuWare E-Invoicing Service, for example, this can be handled automatically via a workflow.

The buyer’s identifier is located through the Peppol Directory, which functions like a directory of all businesses and public authorities that can be reached through the network. The invoice is transmitted to the recipient’s Access Point, where it can be converted into the recipient country’s required format if necessary before being automatically delivered to the recipient’s system.

The 4-corner model illustrated using the DocuWare E-Invoicing Service.

The 4-corner model is designed solely for invoice exchange; the tax authority is not involved. It’s currently used, for example, in Germany and the Nordic countries.

The 5-corner model: including e-reporting

The 5-corner model extends this process by incorporating the tax authority. While the invoice continues to be securely transmitted to the recipient through the Peppol network, the tax-relevant transaction data is simultaneously reported to a government platform in real time. The tax authority reviews these reports, but the invoice continues to the recipient through Peppol regardless of whether the reported data has been processed. Unlike the 3-corner model, no prior approval is required.

The 5-corner model with integrated tax authority reporting (e-reporting) illustrated using the DocuWare E-Invoicing Service.

Because transaction data is reported to the tax authority in real time, the 5-corner model is also known as the Continuous Transaction Control (CTC) model. It is used in countries including France, Belgium, Spain, the United Arab Emirates, and Malaysia. Incidentally, references to 6-corner or 7-corner models generally describe variations of the 5-corner model with additional implementation-specific participants.

DocuWare – future-proof for every model

If you need to exchange electronic invoices internationally while remaining compliant with local regulations, the DocuWare E-Invoicing Service provides comprehensive support for both the 4-corner and 5-corner models. The solution integrates seamlessly into your document processes, enabling both electronic invoice exchange and e-reporting as described above.

As regional legal and technical requirements evolve, DocuWare continuously updates the service. This gives you a future-ready solution that adapts automatically, without requiring you to make changes yourself.